News /

IBC Members' news /

EBRD projects slower growth in Central Asia for 2016 but optimistic for 2017

Lower commodity prices, Russia remittances, slower growth in China continue putting pressure on Central Asian economies

Economies across the EBRD regions are showing modest signs of an upturn after five consecutive years of slowdown, but the recovery expected for 2016 is slightly weaker than forecast six months ago.

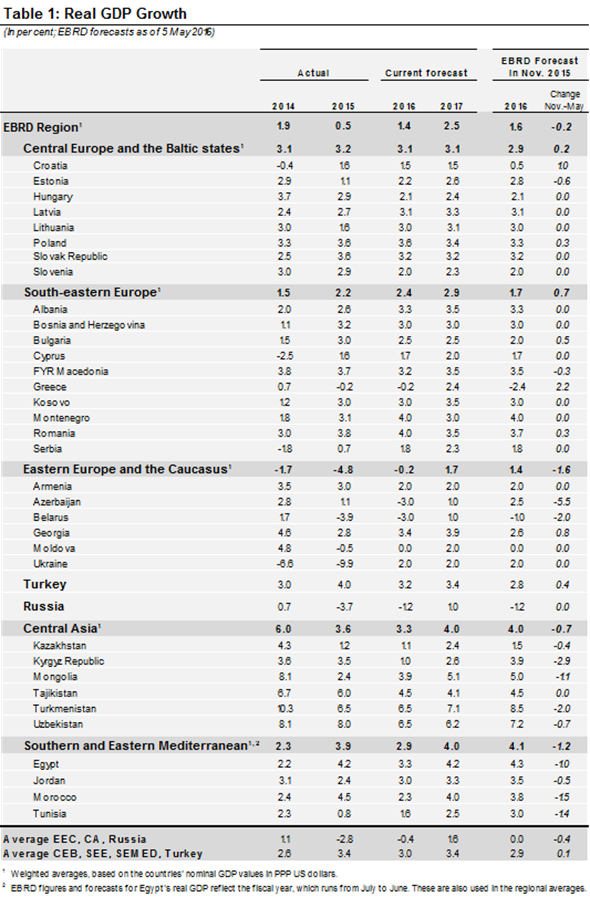

The EBRD’s latest Regional Economic Prospects report sees average growth across the Bank’s 36 countries of operations of 1.4 per cent in 2016, a shade below the 1.6 per cent seen last November, but above the 0.5 per cent result for 2015. A further strengthening is seen to 2.5 per cent in 2017.

Risks to this latest outlook include continuing political tensions, as well the possibility of a sharp deceleration in growth in China, a prolonged weakness in commodity prices and a possible further drop in the price of oil.

The report says weak commodity prices and recession in Russia are continuing to put pressure on the economies of Central Asia and Eastern Europe and the Caucasus. A key factor are lower remittances from Russia.

Forecast for Central Asia

Growth in Central Asia in 2016 is projected to decrease to 3.3 per cent, compared to 3.6 per cent in 2015 and 6.0 per cent in 2014, reflecting expectations of a continuing negative external environment. The countries with the strongest economic links to Russia – the Kyrgyz Republic, Tajikistan and Uzbekistan – are being particularly negatively affected. In Kazakhstan, the largest economy in the region, growth and broader economic conditions, including the exchange rate regime, are expected to stabilize in 2016, following a challenging period in the last quarter of 2015 and the first two months of this year. Growth is expected to reach 1.1 per cent this year, only slightly below the 1.2 per cent achieved in 2015.

The economy is being supported by a combination of a gradual return of investor confidence, stabilisation of the exchange regime internally, private and public investment and more benign commodity prices. FDI from China, including as part of the development of the Silk Road Economic Belt, is providing a significant anchor for growth in some of the countries in the region, and the importance of this source of FDI is likely to increase. Support and investment from Russia also plays an important role.

In 2017, growth in the region is projected to increase to 4 per cent, driven by a positive trend in Kazakhstan in particular, where growth is projected to accelerate to 2.4 per cent. Growth in Mongolia and Turkmenistan, significant commodity exporters, is also likely to improve in 2017. However, a build-up of structural problems over the past two years, resulting from such factors as slowing growth and significant currency depreciation, can be expected to continue to depress growth in the Kyrgyz Republic, Tajikistan and Uzbekistan in 2017.

To read more on the economic forecast for Central Asia, see latest edition of Regional Economic Prospects here http://www.ebrd.com/what-we-do/economic-research-and-data/data/forecasts-macro-data-transition-indicators.html

Rest of EBRD region

Ukraine is expected to return to growth this year. Ukraine should see growth of 2 per cent in both 2016 and 2017 in line with the gradual implementation of structural reforms, after shrinking by close to 10 per cent in 2015.

Economies in Central Europe and the Baltic States (CEB) and south-eastern Europe (SEE), on the other hand, are benefitting from lower energy costs and accommodative eurozone monetary policies.

Growth in Turkey, one of the countries most vulnerable to volatile capital flows, is projected to moderate to around 3.2 per cent this year, from 4.0 per cent in 2015, when it benefitted from a number of one-off factors. The outlook for Turkey has been affected by tourism prospects in the wake of terror attacks and Russian sanctions.

Similarly, the impact of terrorism – as well as a slowdown in global trade -- have led to a significant weakening in the forecasts for the economies of the southern and eastern Mediterranean, where growth is now seen slowing to 2.9 per cent in 2016, a full 1.2 percentage points down from November. A recovery to around 4 per cent is seen for 2017.

Output in Greece is expected to fall slightly in 2016, as investor and consumer confidence remain weak.

In Russia, recession is expected to continue in 2016, with low oil prices and a reduced availability of investment funding leading to a contraction of 1.2 per cent in 2016. Modest growth of 1 per cent is expected in 2017.

The impact of Russia as well as low commodity prices will continue to weigh on growth in Central Asia where growth forecasts have been mostly cut back. The countries with the strongest economic links to Russia are being particularly negatively affected.

News

April 27, 2024: The second meeting of the Kyrgyz-British Business Council was held in Bishkek April 6, 2024: IBC proposals are included in the the Investment Council Action Plan March 13, 2024: IBC Meetup discussed current copyright issues in the IT sector February 28, 2024: IBC signed a memorandum of cooperation with the organizers of the PLUS forum February 19, 2024: IBC will represent the interests of businesses when appealing to the EAEU Court

Hyatt Regency Bishkek Hotel

191 Abdrakhmanov Str.

Bishkek, 720011

Kyrgyz Republic